Ermenegildo Zegna (NYSE:ZGN) Eyes Expansion with Strong Earnings Growth and Strategic Management

Eyes Expansion with Strong Earnings Growth and Strategic Management")

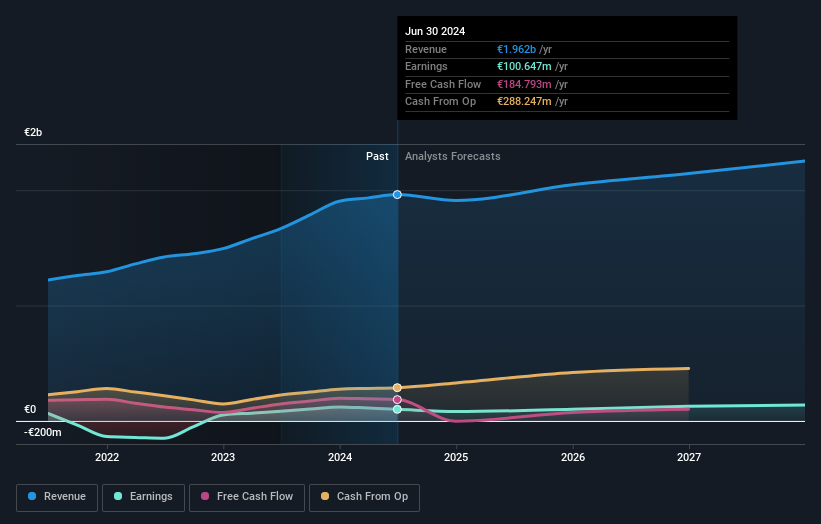

Ermenegildo Zegna (NYSE:ZGN) continues to demonstrate financial resilience and strategic acumen, as evidenced by its recent earnings report for H1 2024, which saw sales increase to EUR 960.12 million, despite a decline in net income. As the company prepares for its Q3 2024 Sale/Trading Statement Call on October 22, investors should anticipate discussions around ongoing product innovation and market expansion strategies, alongside addressing challenges such as lower-than-desired Return on Equity and external market pressures.

Click here and access our complete analysis report to understand the dynamics of Ermenegildo Zegna.

Core Advantages Driving Sustained Success for Ermenegildo Zegna

Ermenegildo Zegna’s recent performance showcases significant strengths, particularly in financial health and strategic management. The company has achieved a remarkable earnings growth of 20.7% over the past year, outpacing the luxury industry average of 11.6%. This is bolstered by a consistent 46.2% annual growth over the past five years. The management’s strategic foresight is evident in their commitment to product innovation, as highlighted by the successful performance of the Thom Browne line, which has resonated well with consumers. Additionally, Zegna’s low net debt to equity ratio of 7.4% and a solid interest coverage of 5.2x by EBIT underscore its financial stability. The seasoned management team, with an average tenure of 13.8 years, provides a strong foundation for navigating market challenges and capitalizing on emerging opportunities.

To gain deeper insights into Ermenegildo Zegna’s historical performance, explore our detailed analysis of past performance.

Critical Issues Affecting the Performance of Ermenegildo Zegna and Areas for Growth

However, certain weaknesses need addressing to sustain growth. The Return on Equity at 12.6% is below the desired threshold of 20%, indicating room for improvement in financial efficiency. Forecasted earnings growth of 11.7% per year falls short of the US market average of 15.4%, and revenue growth projections of 3.5% per year lag behind the broader market’s 8.9%. Moreover, the company’s dividend yield of 1.71% is relatively low compared to top US dividend payers. Despite these challenges, Zegna’s valuation, with a SWS fair ratio of 17.6x, remains attractive compared to industry peers, suggesting potential for market positioning improvements.

To dive deeper into how Ermenegildo Zegna’s valuation metrics are shaping its market position, check out our detailed analysis of Ermenegildo Zegna’s Valuation.

Emerging Markets Or Trends for Ermenegildo Zegna

Opportunities for Zegna include leveraging its experienced management to enhance profit margins and revenue growth. The company’s focus on strategic alliances and product-related announcements can further solidify its market position. With a forecasted earnings growth of 11.73% per year, there is potential for financial stability and expansion into new markets.

See what the latest analyst reports say about Ermenegildo Zegna’s future prospects and potential market movements.

Market Volatility Affecting Ermenegildo Zegna’s Position

Nevertheless, external threats such as economic headwinds and increasing competition in the luxury market pose significant challenges. Supply chain disruptions remain a concern, but Zegna’s proactive risk mitigation efforts are crucial for maintaining operational stability. Analysts’ forecasts indicate uncertainty, which could impact investor confidence. Addressing these threats with strategic foresight is essential for sustaining long-term success.

Explore the current health of Ermenegildo Zegna and how it reflects on its financial stability and growth potential.

Conclusion

Ermenegildo Zegna’s impressive earnings growth and strategic management underscore its strong financial health, positioning it well to navigate market challenges and capitalize on emerging opportunities. However, to sustain this momentum, addressing its below-threshold Return on Equity and improving forecasted earnings and revenue growth are crucial. Despite these areas for improvement, Zegna’s Price-To-Earnings Ratio of 17.6x, which is below both the US Luxury industry average and its peers, highlights its attractive market positioning. This suggests that with strategic foresight in mitigating external threats and leveraging management expertise, Zegna is well-placed for long-term success and expansion into new markets.

Seize The Opportunity

Seeking Other Investments?

“`

Valuation is complex, but we’re here to simplify it.

Discover if Ermenegildo Zegna might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

link

")

")